.png?width=866&height=534&name=Blog%20Banner%20Mistakes%20To%20Avoid%20When%20Registering%20Your%20Insurance%20Agency%20%20(1).png)

Building and maintaining good credit is critical for insurance agents and agency owners. In this article, Financial Coach Alissa Locke identifies five ways your credit can impact the growth and health of your business.

When you’re a busy insurance agent with 400 things on your ‘To Do’ list, reviewing your credit report is probably not high up on your priorities, if it’s there at all! Let’s face it- reviewing your credit is about as enticing a task as getting your teeth cleaned.

And not just your personal credit report! Whether you’re a sole proprietor, an LLC or have incorporated, it’s extremely important to build business credit and monitor this separate credit profile as well. According to Main Street Launch, “There are several advantages to having a separate business credit score. First, it helps you protect your personal credit from a possible business failure.It also works in reverse…Once you’ve built your business score, you’ll have a better chance of raising capital for your small business, either from small-business lenders or credit card companies.”

Monitoring your credit and having a strategy to bolster your credit profile is part of being a good steward of your money and frankly, it can help your business in more ways than you probably realize.

Here are five ways that your credit can impact the growth and health of your business:

1. Hiring Quality Team Members

Credit impacts not only you personally but your ability to hire and license team members. You need to understand how credit works and what is reported on credit reports in case there is something on the new hire’s report that you and they want to dispute. Some good news on this- All three major credit bureaus (Experian, Equifax and Transunion) recently announced significant changes in how they are reporting medical debt which will make the process of hiring and licensing new employees much easier, helping your business hire the best talent.

2. Ability to Qualify for Personal or Business Loans

If you are looking for a business loan, lenders will want to see not only a detailed business plan, revenue history, and what kind of additional collateral the business has, but the lender will look at both the business’s credit score AND the business owner’s credit score, even if you have incorporated your business. And all these factors will go into determining the interest rate on the loan as well.

3. The Rate You’ll Be Offered on Business Credit Cards

Your interest rate, also known as Annual Percentage Rate or APR, will be determined by several factors including the type of loan, your credit score and your risk profile. And the interest rate can be changed at the whim of the creditor on revolving credit! So if you want to get the lowest interest rates, having stellar credit will save you tons of money over time.

4. Where You Can Locate Your Business

We know that having poor credit impacts other areas of your life and your business as well. You already know that credit is used when determining insurance premiums. But credit is also used by landlords to determine if they want to rent to you because it helps them determine your risk level. What if you found the perfect new office space for your business but the landlord reviewed your credit profile and wouldn’t rent to you? Your credit matters.

5. The Added Stress of Poor Credit

Having poor credit negatively impacts virtually every area of your life. Financial worry is a leading cause of mental and physical health issues. Poor credit will cause you to make business and personal decisions that may not be the best. According to CreditRepair.com, poor credit can cause stress, fatigue, anxiety, shame, guilt and anger. In 2020, “19% of adults said their financial burdens impacted their job performance on a monthly basis”. You’ll likely struggle to be the best Agent you can be when you’re dealing with financial strain.

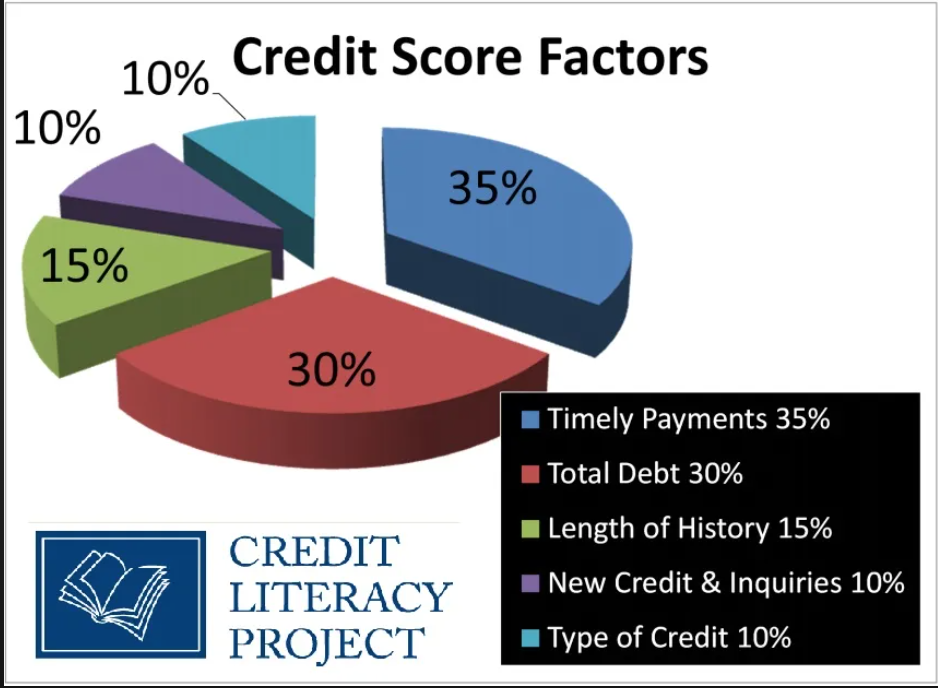

Five Factors That Impact Your Credit Score

According to the Credit Literacy Project, here are the five factors that will impact your credit score and the ‘weight’ of each one:

(Image source: The Credit Literacy Project)

As you can see, paying your bills on time has the greatest impact on your overall score and this is the same for both personal and business credit profiles.

The author of this article, Alissa Locke, is a Financial Coach with Money Mentor Group who specializes in helping insurance agents change their mindset and behavior with their money. As a former SF Agent and Sales Leader, she understands the challenge of trying to budget, control spending, and pay off debt when you're an entrepreneur with fluctuating income and expenses. Money Mentor Group provides one-on-one financial coaching, group coaching, online courses, and tons of free resources, all geared towards helping you understand your relationship with your money.

You can reach out to one of Club Capital’s partners Money Mentor Group to schedule a free introductory Clarity Call with one of their Financial Coaches. They also offer multiple online courses that can take you from confused to confident with your money.

Comments