Most insurance agency owners start out as either an LLC or a sole proprietor. One of the most common questions we receive from insurance agency owners is when they should incorporate the business to file taxes as an S-Corporation.

If your insurance agency is just starting out or has relatively small profit figures, you may wonder whether a corporation is necessary.

When you incorporate your agency, you are establishing a business that is legally separate from its owner. Incorporation turns your sole proprietorship or LLC into a corporation that is formally recognized by your state of incorporation.

The Three Most Common Business Structures for Insurance Agencies

Sole Proprietorship:

The default for any new business selling goods or services. As a sole proprietor you have personal liability, meaning that there is an inherent risk to your personal assets if you run into business debts or liabilities.

The good news is that as insurance agents, liability insurance is usually not hard to come by.

Limited Liability Company (LLC):

A limited liability company is a structured business entity that separates legal liability for your business so you are not personally liable if your agency runs into debt or lawsuits.

LLCs are the easiest entities to establish and maintain and, for most owner-operated businesses, are the go-to entity structure.

Corporation:

Similar to an LLC, a corporation’s structure protects business owners’ personal assets from any corporate liability.

Depending on your individual situation, a corporation may save you money on taxes, or it may cause you to pay more money in the form of opening costs, maintenance fees and, in some instances, more taxes.

C corporations are subject to corporate tax rates, which means that if you’re self-employed, you pay taxes twice (personally and as a business) on the same income source.

To avoid double taxation, most small businesses that incorporate do so as a subchapter corporation, or S corp. S corporations make up over 75% of all corporations in the U.S.

Differences Between a Sole Proprietorship and an S-Corp

There is a cost associated with being an S corp. Corporations have additional recordkeeping and annual reporting requirements that sole proprietorships and partnerships don't have.

Generally speaking, if your agency is profiting less than $50,000 a year, the added costs of being an S corp don’t outweigh the benefits of incorporating.

Should You Incorporate Your Insurance Agency?

Most agents that we work with file taxes as either a Sole Proprietorship or an S Corp

We’ve created an example scenario to compare the implications of filing taxes as a Sole Proprietorship and an S corp.

Home State: Florida

Profit: $100,000

Filing Status: Single

Tax Example: Sole Proprietor

.png?width=1021&name=Club%20Capital%20Taxes%20as%20a%20Sole%20Proprietor%20(2).png)

Tax Example: S Corp

As an S Corp, you must add yourself to payroll and pay yourself a reasonable salary. We’ll use an example salary of $50,000 for this example.

%20(1).png?width=1023&name=Club%20Capital%20Taxes%20as%20a%20Sole%20Proprietor%20(1024%20%C3%97%201568%20px)%20(1).png)

In this example, filing taxes as an S-Corp instead of Sole Proprietor would save you $4,973.

Comparison of Benefits: S-Corp and Other Forms of Business

Benefits of an S Corp vs Sole Proprietorship

- Personal asset protection

- Unlimited existence

- Easier to transfer ownership of the business

Benefits of an S Corp vs LLC / Partnership

- LLC Members / Partners cannot be employees

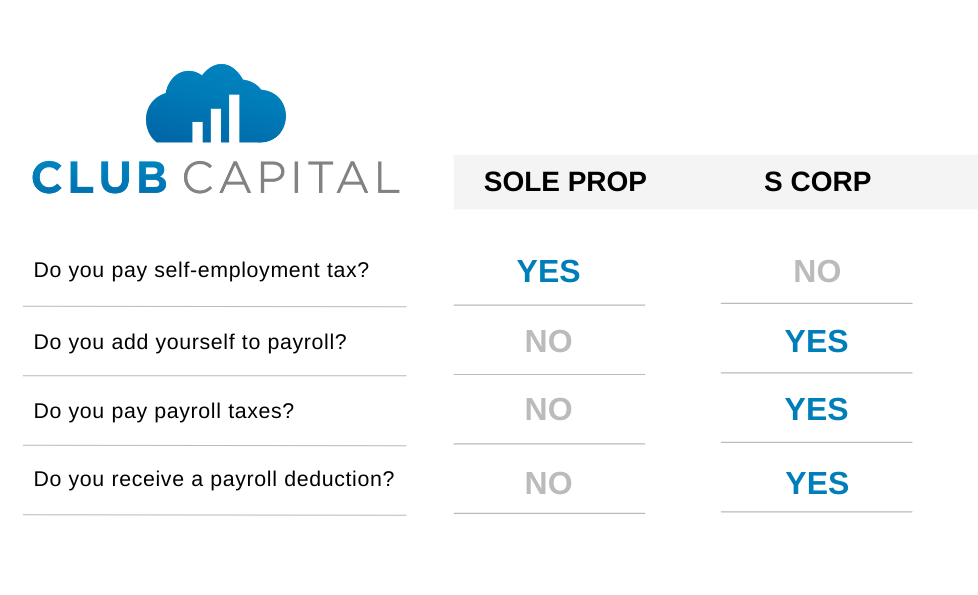

- S-Corp profits are not subject to self-employment taxes

Benefits of an S Corp vs C Corporation

- Flow-through taxation avoids corporate income tax

Added Costs For An S Corp

There are great benefits to S corporations that can help save you money, but it may also be costlier overall. Similar to a large corporation, an S corp has both initial and ongoing accounting and legal costs. Depending on the state the corporation was formed in, some states also require S corps to pay ongoing maintenance fees such as Annual Reports and Franchise Tax.

Added costs for S Corps include:

- Salary

- Employer payroll taxes

- Payroll service fees

- Bookkeeping and accounting fees

- Tax preparation

- Annual state registration fees

If you are considering switching to an S corp, make sure the savings outweigh the added costs.

Consider These Factors For Your Insurance Agency

Consider these legal components before switching your agency to an S corp.

- Your insurance license needs to change appropriately when you incorporate.

- Your agency needs to be contracted by it’s revenue source.

- Make sure the parent company is able to contract with your new entity.

Deciding the Right Business Structure for Your Agency

There are many benefits to incorporating your insurance agency, from receiving limited liability protection and lessened tax responsibilities when you elect a pass-through entity to building business credit and establishing credibility with clients.

Do the benefits of being an S corp outweigh the added costs for your insurance agency? With so many factors to consider, we recommend speaking with one of our Tax Experts for personal one-on-one support.

Comments